Savings Account Germany

Last update: 14 February 2023

So you’re settled in Germany and have put some money aside? Good on you! But know you might ask yourself where to put your money… Of course you could just leave it on your normal bank account, but chances are high that it then somehow disappears. And by “disappear” I mean you spend it for shopping, partying and so on 🙂 If you want to avoid this, it makes sense to put this money on a separate savings account. In this article we are going to describe what options you have and give a comparison of the best German savings accounts.

Topics Overview

hide

What types of savings accounts are there in Germany?

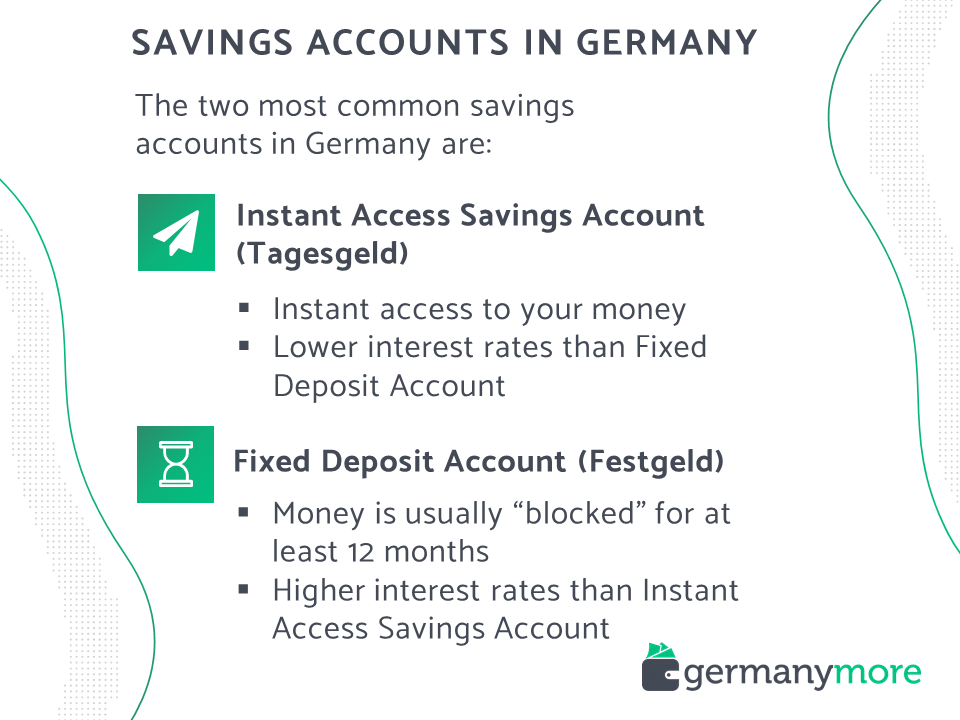

Instant access savings account – in German “Tagesgeldkonto”

The instant access savings account is probably the most common savings account in Germany. As the name says, you can access your money instantly, which means you can transfer it whenever you want from your savings account back to your normal bank account. Interest rates are usually higher than on your normal bank account (if there are any…) but lower than on a fixed deposit account (see more in next paragraph). Below you can find a comparison of the best German instant access savings accounts:

Fixed deposit account – in German “Festgeldkonto”

Unlike the instant access savings account, you cannot dispose of your money instantly with the fixed deposit account. Usually your money is “blocked” for at least 12 months up to a few years. Of course it’s your decision, for how long you want to invest your money. Because of the longer investment period, interest rates are higher than for the instant access savings account. Here is a comparison of the best fixed deposit accounts in Germany (you can select your investment period under “Anlagedauer”):

Is my money safe?

Generally speaking… yes. For bank accounts within the European Union there is a general deposit insurance of 100.000 EUR per bank account. Most of the above bank accounts presented in the above comparisons are located in the European Union.

For most German savings accounts, the deposit insurance is even higher. For example the deposit insurance of TARGOBANK covers deposits of up to 405.007.000€. Yes that’s correct… over 400 million Euros! So absolutely nothing to worry about.

How does it work with taxes?*

Well, taxes in Germany… Definitely a difficult story! The money you make with your savings account in Germany is classified as income from capital (in German “Einkünfte aus Kapitalvermögen”). For this type of income there is a flat tax rate of approx. 26% (the so-called “Abgeltungssteuer”). So for every Euro you make from interest, you have to pay 26 cents taxes. However there is an allowance of 1,000 EUR per year, which means that the first 1,000 EUR earned from interest are tax-free. For more details on the taxation of income from your savings account, you can check this Wikipedia article.

You are still wondering how to submit a tax return in Germany? Learn in this article which options you have for submitting your tax return.

Instant access savings account: flexible, safe, more profitable

There are reasons for the popularity of the instant access savings account: Unlike a savings account in Germany, you as a customer have complete flexibility with an instant access savings account or call money account. You can move as much money as you want at any time – there are no monthly limits or notice period with overnight money.

Perhaps the most important advantage of instant access over savings accounts, however, is that interest rates are usually somewhat higher. Furthermore, with many overnight deposit models, the banks in Germany pay interest on the deposited amount every month or every quarter – this creates compound interest effects that improve the effective interest rate.

Otherwise, all the advantages of the savings account in Germany can also be found in instant access savings accounts. For example, the security of the investment is just as high. Also, you usually do not have to pay fees for account management or for opening a call money account. There is usually no minimum deposit either.

Open and close a savings account in Germany: Online or at a bank branch?

If you want to open a savings account in Germany, you have two options: online or directly on site at the bank branch. You basically only need your ID card to complete the formalities. Also note that some banks require a (usually small) initial deposit as well as a minimum deposit – so you should have some cash on hand for an initial deposit. Furthermore, there are providers who charge penalties if their savings account does not have a certain minimum deposit.

When opening a savings account online, you enter your data in the appropriate fields of the application form. If you are already a customer of the bank where you want to open the savings account with passbook, you may not need to enter all the data again. The actual contract is usually sent to you by mail, it becomes valid only after you sign it. New customers must prove their identity in accordance with the requirements of the Money Laundering Act (GwG) – in most cases this is done using the so-called Postident procedure. The documents required for this are usually sent to you with the contract documents. At the post office, you will have to identify yourself, and then the postal employee at the counter will confirm your identity. Once all the documents have been received, the savings book – if a physical book is part of the contract – will be sent to you by mail.

Or customers use the increasingly popular VideoIdent procedure. VideoIdent is short for video identification and is also a procedure for confirming a person’s identity online. The online legitimation has already been approved by BaFin since 2014 and is carried out via video chat. With the help of a webcam on the computer or a smartphone or tablet and a valid identification document, the customer receives a link from the bank, whereby he is redirected to a corresponding page. There, the VideoIdent procedure is then carried out by an employee of the company.

Unless you are a customer of a direct bank, you can also simply open your savings book at a bank branch. A bank employee will go through all the points of the account opening application with you, and you will identify yourself with your ID card. The advantage of this procedure: Any questions are clarified directly on the spot and you can take your savings book with you immediately.

Time deposit: Long commitment, higher yield

The great benefit of this long-term commitment with a fixed-term deposit: Interest rates are fixed for the entire term – and are generally higher than for savings accounts and overnight deposits in Germany. Potential fluctuations in interest rates, as is the case with overnight deposits, do not occur with fixed-term deposits due to the fixed interest rate. The exact amount of interest varies slightly from provider to provider, but is generally based on the market interest rate. Basically, the conditions depend on the term and the amount paid in. The longer you commit and the more money you invest, the better the interest rate conditions are as a rule for a fixed-term deposit account in Germany.

Instant access and fixed-term deposits: How the accounts in Germany work

Call money and time deposit accounts work via a reference account – this is usually your checking account. Accordingly, you must provide bank details when opening an account. Cash deposits and withdrawals are not possible with these German accounts; all transactions are processed via the reference account. There are usually no fees for bookings.

If you want to open a reference bank account first, check out our comparison of the best German bank accounts.

Thus, deposits to a call money account are made by transfer from your reference savings account in Germany. Note, however, that the call money is only a credit account – you cannot pay bills via this account, for example. If you want to withdraw money from your call money account, you must transfer it to the reference account. Cash withdrawals are not possible. Although the overnight deposit account is considered a very flexible investment, you do not have immediate access to your money.

With the time deposit account, you pay the amount to be invested into the account after signing the contract. Over the entire term, the amount remains untouched, so there are usually no transactions.

Summary – Savings Account Germany

This should give you a good overview of the options that you have for a savings account in Germany. Should you still be looking for a normal bank account, check out this article that gives you a good comparison of bank accounts in Germany.

Disclaimer:

*With regards to the section “How does it work with taxes?”, this is no official tax advice and just a general information about the taxation of income from interest. I’m not a professional tax advisor. If you need assistance please get in touch with an official tax advisor.

This post contains affiliate links, meaning I earn a commission if you use those links.